So let’s say you have a great business idea, you’re willing to take some risks (leave your current job and work from your home office, for instance) but no matter how good your idea is, there’s surely one hurdle stopping you – you don’t have enough money.

Ok, you’ve probably heardabilliontimes that around 90% of startups are destined to fail during the first few years.

In reality, things aren’t as bad as people make them up to be. In fact, according to research from the US Bureau of Labor, more than 75% of new businesses in the United States survive the first 12 months and around 50% make it to five years.

Now, money shouldn’t be the reason a great idea get shelved, however, lack of finances is one of the main reasons why young and up-and-coming entrepreneurs put their plans on hold.

Why do you Actually Need Money?

So why do you need a ton of money in the first place?

For starters, you need to understand that there is no “universal fee” for starting a business. Simply put, different businesses have different needs and some businesses need more money to stay afloat during the first few years than others.

Here are a couple of things you need to consider:

- Equipment– Does your business require any specialized hardware or software?

- Supplies – Do you need new machines, computers or raw material?

- Operating Expenses– In addition to standard expenses, think about the marketing expenses.

- Legal Fees – Do you need any special paperwork to operate your business?

- Employees – If you cannot work by yourself, how many people you need?

With that in mind, there are actually two paths of starting a business with a micro-budget – cutting back on expenses and get funding from outside sources.

Four Ways to make Your Startup Successful

1. Cut the Unnecessary Costs

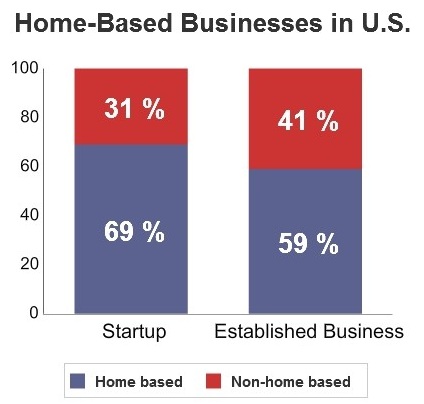

At first, you probably won’t have enough money and resources to attract the top talent. So if you have to hire a couple of people, make sure to hire the ones who could quickly lean a task and solve problems. But another option is to start running your operation by yourself to eliminate additional costs. Image Source: https://smallbiztrends.com

Image Source: https://smallbiztrends.com

According to a recent Global Entrepreneurship Monitor report, almost 70% of entrepreneurs do the same. And that’s not just during the startup phase, almost 60% of business owners continue to operate their companies long after their businesses are up and running.

2. Revise Your Business Model

Once you decide to start working as a solopreneur, you need to change your business model to demand even fewer needs. So unless an office is crucial for your business, you can actually work from home. Also, you should find cheaper sources of supplies, or even cut entire product lines that are too expensive to produce.

Of course, there are some expenses you won’t be able to avoid, such as legal fees, licensing, etc. – they will set you back a couple of thousands, even if you manage to cut back on every single expense. But don’t worry; according to Small Business Association, most micro-businesses get started on around $3000, and home-based business can be started for only around $1000.

3. Look Into Crowdfunding

According to Entrepreneur, almost 80% of startups today are self-funded, and almost a quarter of them (roughly 24%) find funding from family and friends. But if your family isn’t willing to lend you some money, you still have another option – crowdfunding.

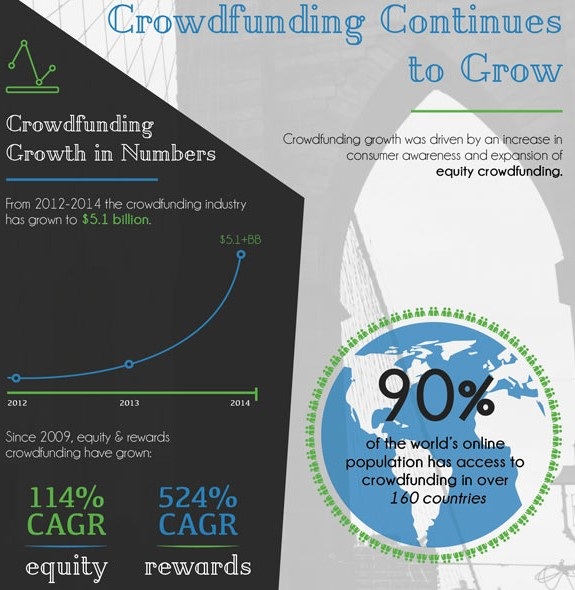

Image Source: www.entrepreneur.com

And while only around 3% of startups use crowdfunding, the crowdfunding industry itself has grown dramatically in the last couple of years. Today, the crowdfunding industry is worth more than $5 billion and it raises more than $2 million each day.

4. Find Angel Investors or Venture Capitalists

So what are angel investors exactly? Well, even though we don’t have an official definition, they are usually wealthy individuals who back up new companies early in their inception. But you have to be aware that these individual also invest in exchange for partial ownership of the organization, but that’s a sacrifice well worth considering if you’re working with a zero budget.

Another option you have is find some venture capitalists, which are very similar to angel investors. However, they are typically organizations that tend to scout companies that are already in existence. And if you don’t know where to start, it would be wise to look up companies like Asset Finance Shop that provide commercial financial services and can get you in touch with potential investors.

Final Thoughts

With those four options, you should be able to cut your financial investment to almost zero. Nevertheless, you may have to take some other sacrifices (starting really, really small is definitely one of them) – but if you believe in your business idea – none of these sacrifices should stand in your way to success.